Geo-specific Complexities of Regulatory Compliance for Banks

Navigating the geo-specific regulatory compliance for banks is no easy feat. Learn how to stay updated on changing global banking regulations.

As many large banks and financial institutions extend their operations and offerings globally, their regulatory compliance obligations increase in complexity, exposing your organization to a greater degree of compliance risk than ever before. Regulations change in the hundreds daily, and the geo-specific nuances in common compliance regulations for banks, like Anti-Money Laundering (AML), GDPR, and NIST, mean teams have little time to ramp up on regulatory compliance change management. This inevitably increases the cost of doing compliance well.

For banks, regulatory compliance is a complex and ever-evolving challenge. With different regulations in different countries, geo-specific complexities can make the work of compliance teams even more difficult. In this blog post, we’ll explore the key examples of geo-specific regulatory compliance complexity and how to set your team up for success.

Regulatory compliance for banks: Frameworks and bodies

At the root of regulatory compliance for banks is a desire to put customer information safety first while also reducing incidents of bank fraud and crime. In the U.S., banks need to be Sarbanes-Oxley (SOX) compliant, which came into law after the global financial crash of 2008. The Office of the Superintendant of Financial Institutions (OSFI) regulates and supervises domestic and foreign banks operating in Canada. Regulatory compliance for banks in the European Union is set by the European Banking Authority (EBA). With Brexit, compliance teams need to roll out what most are referring to as U.K. SOX, which brings Britain closer to U.S. federal banking regulations and protections in terms of audit and governance reform.

Overall, these regulations have been created with one purpose in mind: protecting customers from harm while ensuring that bank fraud is minimized or prevented altogether. Compliance teams now face an ever-changing landscape due to new laws being implemented across different countries —making their jobs more challenging than ever before. Fortunately, new solutions are available which can simplify risk management and free up time for compliance teams so they can focus on results rather than getting bogged down in minor details.

Navigating the complexities of regulatory compliance is no easy feat for banks, particularly when it comes to geo-specific regulations. With ever-evolving international banking laws, compliance teams are often tasked with staying up-to-date on the various regulations in different countries. Fortunately, there are solutions available that can simplify compliance risk management processes and free up compliance teams to focus on results.

Data transfer

Data transfer is a critical component of regulatory compliance for banks, as it involves the transmission of sensitive financial information between countries. Any data transfers that are not compliant with the laws and regulations of both the sending and receiving countries can incur potentially hefty fines or other penalties.

This makes understanding the various geo-specific complexities of regulatory compliance for banks and other organizations paramount when engaging in international data transfers. The laws regulating data transfer vary widely from country to country, making it difficult to keep track of all the different requirements and restrictions.

For example, many European countries have strict privacy laws that require companies to take extra measures when transferring personal data out of the European Union (EU). Companies must meet the standards set forth by the General Data Protection Regulation (GDPR) if they wish to transmit any information about EU citizens outside its borders. Additionally, each individual EU member state may have additional data protection laws that must be considered.

Aside from privacy regulations, there may also be restrictions on foreign currency transfers or limitations on how much money can be sent abroad at one time — particularly in cases where sanctions are in place against certain nations or regions.

Know Your Customer (KYC)

Banks have the sole responsibility for validating that a customer is who they say they are. As an organization’s global customer base and transactions grow — and as regulations expand to cover new ways of moving capital — the need to monitor regionally changing regulations in this space is critical.

The Know Your Customer (KYC) process is a critical part of regulatory compliance for banks; it allows organizations to identify and verify the identity of customers. This process has become more complex over the years, as regulations have been updated to cover new ways of moving capital across borders and as organizations’ global customer bases have grown. Banks must remain vigilant in keeping up with changing regional regulations to ensure they are compliant with them.

To meet these constantly changing expectations, banks must develop robust internal processes for dealing with KYC requests efficiently while maintaining secure systems for storing customer information safely and securely. Modern technology solutions can help simplify this process by automating many manual steps involved in verifying customer identities while allowing for greater control over how their data is used and stored.

Cross-border banking and lending

Cross-border banking and lending can be one of the most complex aspects of regulatory compliance for banks. U.S. banks specifically must understand not only the regulatory requirements of their country but also those of any countries with which they transact business. This is especially true when it comes to currency financing, as different countries have different rules that must be followed to comply with both local and international regulations. For example, if a U.S. bank provides a loan to an individual or business in Switzerland, it must understand the Swiss banking regulations for money laundering prevention and other financial compliance factors such as capital adequacy requirements to remain compliant with both nations’ laws.

Banks also need to consider the tax implications of conducting business across international borders because different countries may have different tax rates and reporting requirements for transactions involving citizens of other nations. Failure to do so could lead to hefty fines or civil suits against the bank for noncompliance with applicable laws and regulations related to international taxation matters.

Capital markets

Capital markets are subject to increasing levels of complexity from a regulatory compliance perspective. With the rise of digital trading, transactions can be completed in nano-seconds, leaving investment companies and banks with investing arms vulnerable to money laundering and other forms of financial crime.

Regulatory bodies such as the Financial Conduct Authority (FCA) in the U.K. have issued specific guidance on how firms should conduct their business to remain compliant with anti-money laundering regulations. Banks must also ensure that they have the appropriate personnel trained and knowledgeable about current regulations so they can effectively assess risks associated with money laundering activities. While new technologies can help automate many manual processes associated with compliance, having a competent team of experts is essential for overseeing these activities and ensuring that regulatory requirements for banks are met at all times.

Structured financing

Structured financing can be a complex undertaking for any company that requires international collaboration. If a company seeks to finance a project in South Africa with shareholders or investors from Brazil, Norway, Australia, and South Africa, the financial regulations of each country must be taken into account. The compliance team must create a thorough understanding of the taxation rules and regulations, capital adequacy standards, money laundering prevention measures, economic sanctions, and other related laws in each respective county.

With the right technology tools in place, compliance teams are freed up from managing tedious manual processes so they can focus more on achieving results instead of getting stuck in the weeds of complex regulatory compliance for banks.

Do your due diligence

In terms of cross-border regulatory compliance for banks, do your due diligence to identify the nature of the parties involved in the transactions by asking:

- What are the nationalities of the persons and entities involved?

- Is this a situation where beneficial ownership should be considered?

- Could the transaction reveal a conflict of interest due to ownership or control by politically exposed persons?

When it comes to regulatory compliance for banks, geo-specific complexities can make the work of compliance teams especially challenging. Depending on the type and scope of transactions, banks may be required to adhere to multiple sets of regulations in different jurisdictions. Before any transaction is executed, banks need to do their due diligence and identify the nature of the parties involved.

One key factor to consider is the nationality of all persons and entities associated with a transaction. Banks must understand if they are dealing with clients from different countries or regions and how those jurisdictional differences affect their operations. In certain instances, beneficial ownership should be taken into account as well. This includes investigating who ultimately owns or controls a company or legal entity involved in a transaction.

In addition, banks must take care not to enter into deals with Politically Exposed Persons (PEPs). PEPs are individuals who hold public office or have close ties with government officials. All transactions involving them must be carefully scrutinized for potential conflicts of interest. To this end, knowing who holds positions of influence over any entity being considered can help ensure that financial institutions comply with relevant laws and regulations in each country where they operate.

Ultimately, understanding these geo-specific complexities is essential for ensuring proper regulatory compliance for banks around the world. By taking time to research the backgrounds and affiliations of all parties involved in a transaction before signing off on it, banks can avoid costly fines and reputational damage related to non-compliance while still delivering value to customers across borders.

Set your team up for regulatory compliance success

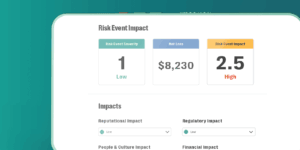

Compliance teams are the first line of defense in mitigating non-compliance risks. With the right tools, they can be empowered to stay informed and ahead of any changes to rules and regulatory compliance for banks. Resolver’s Compliance Management software offers an intuitive user interface that gives teams access to the most up-to-date information at their fingertips, allowing them to easily identify areas where their compliance posture may need improvement.

Our platform gives compliance professionals the confidence to provide an opinion of the organization’s state of compliance through meaningful data and increased visibility into all compliance efforts. From automating regulatory change management to reducing compliance fatigue and giving teams the power to visualize their full regulatory compliance environment, our highlight flexible solution can grow and scale as your compliance program’s maturity does.

Resolver’s Compliance Management solution is designed with scalability in mind — offering flexibility to grow and mature alongside your organization’s compliance program needs as they evolve. From automating regulatory change management processes to improving visibility into your overall regulatory environment, our team of experts will help you set your team up for success so you can focus on generating meaningful results from your compliance efforts. Watch our webinar, Transforming Regulatory Complexity into Risk Intelligence to see learn more.